You did everything right.

You did everything right.

You sat down with an attorney. You signed the documents. You made sure your spouse, or your adult child, or your trusted sibling knew where everything was kept. You told yourself your family would be protected if something happened to you.

Then something happened.

And the bank said no.

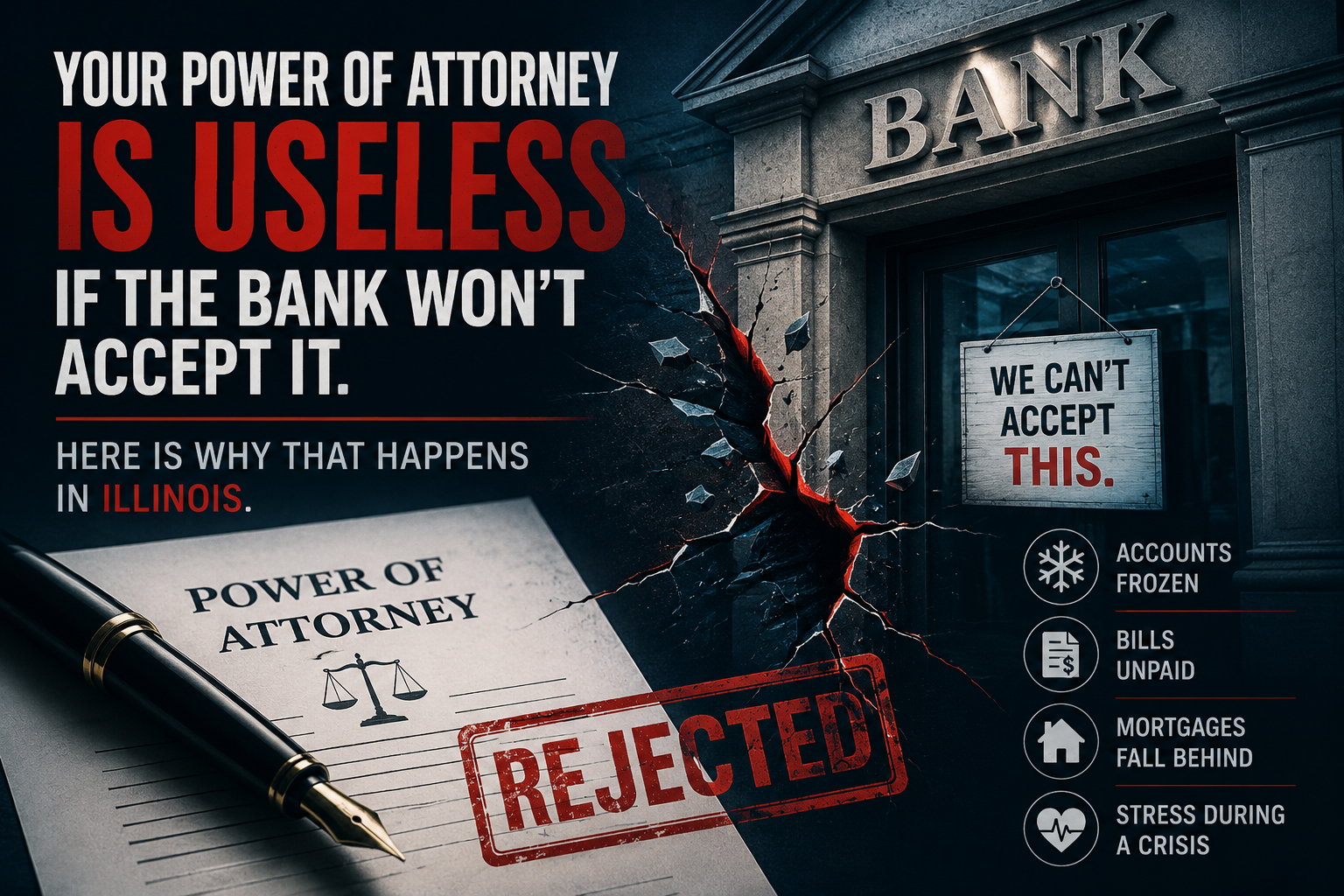

This scenario plays out in Illinois more often than most people realize. A loved one becomes incapacitated, a family member shows up at the bank with a properly signed Power of Attorney document in hand, and the bank refuses to honor it. Accounts stay frozen. Bills go unpaid. Mortgages fall behind. The stress of a medical crisis collides head-on with a financial brick wall, and the document that was supposed to prevent all of this is sitting on a desk doing nothing.

If this has happened to your family, you are not alone. And if it has not happened yet, what you do not know about your Power of Attorney could cost your family significantly when it matters most.

What a Power of Attorney Is Supposed to Do

A Power of Attorney for Property is a legal document that authorizes someone you trust, called your agent, to manage your financial affairs if you become unable to do so yourself. It is one of the most important documents in any estate plan, and in many situations it is more immediately useful than a will.

A will only matters after you die. A Power of Attorney for Property matters while you are alive but incapacitated. Stroke. Dementia. A serious accident. A prolonged illness. These are the moments your Power of Attorney is supposed to step in and keep your financial life from unraveling while your family focuses on your care.

When it works, it is seamless. When it does not, the alternative is a court-supervised guardianship proceeding that is expensive, time-consuming, and entirely public.

Why Banks Refuse to Honor Them

The frustrating reality is that banks have historically been reluctant to accept Powers of Attorney, even valid ones. Their reasons vary, and not all of them are legally justified.

The document is too old. Banks have no obligation under Illinois law to refuse a Power of Attorney simply because it is several years old, but many do it anyway. Some have internal policies requiring documents to be no older than a certain number of years. If your POA was signed a decade ago, some institutions will push back regardless of whether it remains legally valid.

The bank cannot verify it. Financial institutions are understandably cautious about fraud. An agent showing up with a document, claiming authority to access someone else’s accounts, raises compliance flags. If the institution cannot quickly verify the document’s authenticity or the principal’s current status, refusal is often the default.

The document has technical deficiencies. A Power of Attorney signed without proper witnesses, or using a form that does not comply with Illinois statutory requirements, can give a bank legitimate grounds for refusal. Online forms and DIY documents are a common source of this problem.

The agent’s authority is unclear. Illinois Power of Attorney documents allow for significant customization. An agent who shows up without a clear understanding of exactly what powers have been granted, or with a document that does not spell out specific authorities in sufficient detail, may face pushback.

The bank is being overly cautious. This is the most aggravating scenario, and it happens regularly. The document is valid. The agent has authority. The bank refuses anyway, either due to internal policy confusion, employee unfamiliarity with the document, or simple institutional caution.

What Illinois Changed in 2025 (And Why It Matters Now)

Illinois took a significant step toward fixing this problem when Governor Pritzker signed Public Act 103-0994 into law. The amendment took effect January 1, 2025, and it directly addresses the problem of financial institutions unreasonably refusing to honor Powers of Attorney.

Here is what changed.

The law now establishes a formal framework distinguishing between reasonable and unreasonable grounds for a third party to refuse a Power of Attorney. Banks and other financial institutions can no longer simply decline a properly executed document without legal consequence. The law specifically defines what constitutes an unreasonable refusal, and institutions that refuse without justification face civil liability for any resulting damages.

At the same time, the amendment gives institutions a new tool. A bank can now request that the agent provide a written certification, under penalty of perjury, confirming that the Power of Attorney is still valid and that the agent’s authority is currently in effect. This Agent’s Certification and Acceptance of Authority gives the institution protection while giving agents a clear, legal mechanism to move the process forward.

What this means practically: if you are an agent whose Power of Attorney is being rejected by a bank, you now have a specific legal path to push back. And if you are someone who has a Power of Attorney in your estate plan, the 2025 amendment is a strong reason to review that document with an attorney to make sure it is structured to hold up under the new framework.

The Situations Where This Breaks Down Most Often

Even with the 2025 amendment in place, there are circumstances where Power of Attorney rejections continue to cause serious problems for Illinois families.

When the document was drafted without an attorney. The internet is full of Power of Attorney templates. Some of them are technically compliant. Many are not. A document that was downloaded, filled out, and signed without professional guidance frequently lacks the specificity that financial institutions need to act on it confidently.

When the agent and the institution are meeting for the first time. If the principal has an existing relationship with a bank but the agent does not, the institution has no history with this person and no context for the claim of authority. The new certification process helps here, but agents who are unfamiliar with the process still run into delays.

When the principal is already incapacitated and cannot confirm the grant of authority. This is the worst possible time to discover a problem with your documents. Once someone lacks capacity, they cannot execute a new Power of Attorney. The document that exists is the document you have to work with. If it is deficient, the only alternative is going to court.

When real estate or investment accounts are involved. Banks are cautious. Brokerage firms and title companies can be even more so. Powers of Attorney that are perfectly acceptable for basic banking transactions are sometimes rejected when real estate transactions or investment account management are involved, because those institutions have their own compliance standards layered on top of state law.

What You Should Do Right Now

If you already have a Power of Attorney, the 2025 amendment makes this a good time to have it reviewed by an estate planning attorney. Specifically, you want to confirm that it was properly executed under Illinois law, that the scope of authority is clearly defined, and that it includes the language that gives your agent the best chance of being accepted by financial institutions without a fight.

If you are the agent under a Power of Attorney and a bank is refusing to honor it, do not simply walk away. The 2025 law gives you a legal basis to push back. An attorney can help you prepare the Agent’s Certification and Acceptance of Authority, communicate directly with the institution’s legal or compliance department, and if necessary, take legal action against an institution that is refusing without reasonable cause.

If you do not have a Power of Attorney at all, the answer is simple. Get one. The alternative, if you become incapacitated without one, is a court-supervised guardianship that costs thousands of dollars, takes months, and puts your private financial matters into public court records.

A Note on Healthcare Powers of Attorney

Everything above applies primarily to the Power of Attorney for Property, which covers financial decisions. Illinois also has a separate Power of Attorney for Healthcare, which authorizes an agent to make medical decisions if you cannot make them yourself.

Healthcare Powers of Attorney face a different set of institutional resistance issues, primarily in hospital and care facility settings. That is a topic worth its own discussion, but the same foundational principle applies: a document that has not been properly drafted and executed is a document that may not work when your family needs it most.

The Bottom Line

A Power of Attorney is only as useful as its ability to be honored when the moment comes. The document sitting in a folder in your filing cabinet may give you and your family a false sense of security if it has not been reviewed by an attorney who understands what Illinois institutions actually require in practice.

The 2025 amendment to the Illinois Power of Attorney Act was a real improvement. But it did not eliminate the problem. It created a framework. Navigating that framework still requires knowing your rights and being prepared to assert them.

The families who come through these situations without a crisis are the ones who planned ahead with documents that actually work, and agents who know what to do when they walk into that bank.

Tracy Ries Helps Illinois Families Get Estate Planning Right

Tracy A. Ries is an estate planning and probate attorney at Bellas and Wachowski with over two decades of experience helping individuals and families in the Chicago area protect what matters most. She works with clients to draft Powers of Attorney that hold up in the real world, not just on paper, and she guides agents and families through the process when institutions push back.

If your Power of Attorney has not been reviewed recently, or if you are an agent facing resistance from a bank or financial institution, call for a consultation before the situation becomes a crisis.

Call 800.825.9260 or contact Tracy directly at tracy@bellas-wachowski.com.